What Will Happen With Insurance In 2026?

Happy New Year and Welcome to 2026!

A couple weeks ago, a Realtor that I know asked me for a prediction of what will happen with insurance in the coming year. Before we look forward, let's take a quick look back. In 2023, Ricardo Lara, the CA Insurance Commissioner required insurance companies to start offering discounts for hardening your home. While this was a great idea, the execution and delivery of real savings was not that good. This was potentially the start of something good though. We will circle back to this in a bit.

In September 2023, Ricardo Lara, announced the multi-point plan to improve the states market conditions, in an effort to get insurance companies to start writing more policies. After about 2 years, there are 6 insurance companies, Mercury, AAA, USAA, Pacific Specialty, California Casualty and the CA Fair Plan, which have agreed to get on board with using one of the two approved wildfire risk mapping systems the Department of Insurance is allowing every insurance company to use, in order to file their rates. To put this in perspective, there are 100-120 admitted home insurance companies, who file their rates with the state. To be clear, there are only 6 who decided to file their rates with the new tools.

This leads us to...what will happen in 2026?

If the LA-area fires had not happened a year ago, we would be in the same position we are in now. Most insurance companies are ready to write home insurance...again. Of course, there are some exceptions who are not quite ready, like State Farm or Allstate. I have heard rumors that State Farm will return in 2026, but I have also heard 2027.

For the companies that are back open for business, most will only offer home insurance, if it is packaged with car insurance. Historically and economically speaking, insurance companies know their numbers. If the home insurance is not making them money, then the car insurance is or vice versa. Insurance companies books are better balanced when they have the whole package; car and home. The good news is, insurance companies are back and want to write new business.

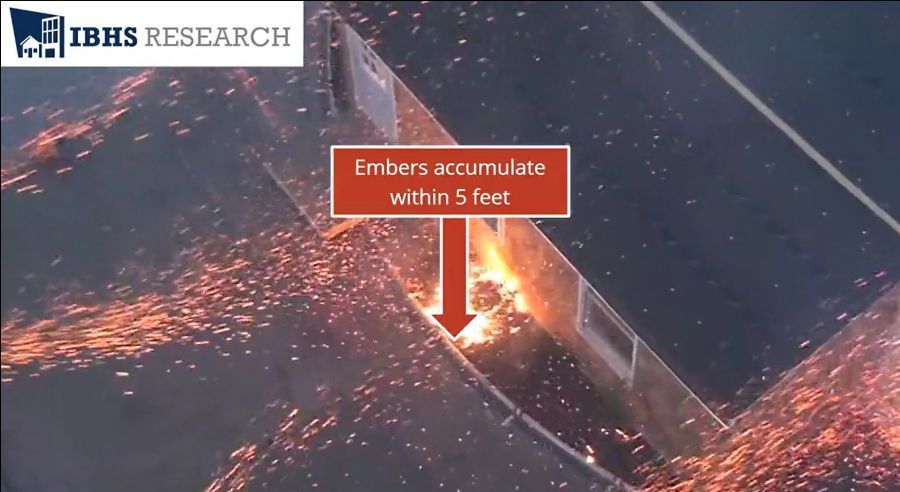

What we are also seeing is insurance companies are starting to expect their clients to do some preventative maintenance, like installing automatic water shutoff valves or hardening your home (changing your vents to make them more ember resistant, removing bushes, mulch and other flammable items close to your home).

As we progress through 2026, we hope insurance companies continue to loosen their underwriting guidelines for the age of homes. Some companies are holding at 30 years of age or newer and others are moving to 50 years old, while others have a 100+ year old limit.

We do not see wildfire guidelines loosening and the CA Fair Plan keeps growing since "normal" companies no longer write in higher fire areas. The Fair Plan is working on making itself more financially stable by being able to purchase a catastrophe bond.

In my opinion, I believe 2026 is moving in the right direction for insurance. More options, more companies saying "yes." This is good news!

Subscribe for More

Sign up in the Stay Informed section below to get on our list for more helpful tips and information.