By Aaron Rosen

•

May 18, 2026

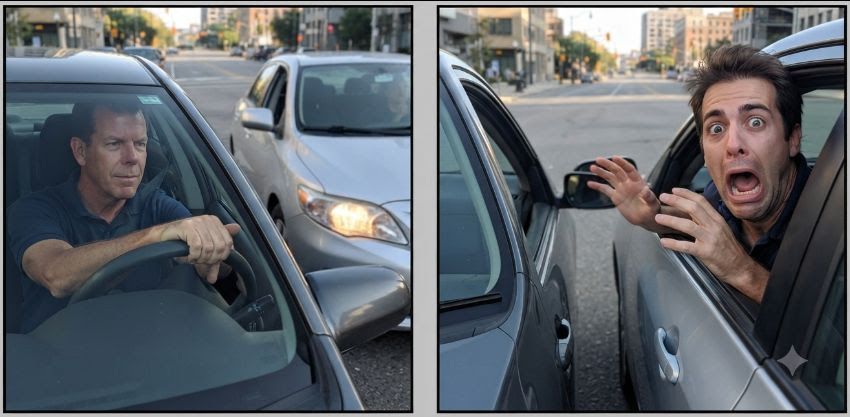

When you see an accident like this, it kind of makes you wonder, who is at fault? I drove past this accident, just last week. At first glance, I could not tell who hit the light pole. And then, I figured it out. What do you think? Who is at fault here? What you cannot see in the picture is that the truck had damage on its rear, leading me to believe the Audi, rear ended it, pushing it into the light pole. If you were the driver of the truck, you may be responsible for paying for the property damage for the light pole, even though the Audi pushed you into it. The good news is, if you are responsible, your insurance company should be able to recoup the money from the Audi's insurance through a process called subrogation. Subrogation is the legal right of an insurance company to seek reimbursement from a responsible third party, after paying a policyholder's claim. We receive a lot of calls from clients about car accidents. First, we want to make sure everyone is ok. Second, we want to know, who caused the accident. If our client did not cause the accident, we have found it best to file a claim against the responsible parties insurance and have them handle all the payments, rental car, etc, directly with you, instead of filing a claim on your own insurance. It helps prevent your insurance company from having to subrogate the claim. It also keeps your record cleaner, with your insurance and helps reduce the possibility of rate increases due to accidents that are not your fault. While insurance companies are not supposed to increase your rates due to not at fault accidents or comprehensive claims, they would also prefer to not pay for them either, as it is their time, people and money to pay those claims. There are times when you may need to involve your insurance company, because the other party is not cooperating. And that is 100% fine. If you can avoid it though, in my opinion, you are better off. For now, drive safe, stay alert, look both ways before proceeding on a green light and as always, if you have any questions, we are here to help.